Westward Gold Generates New Targets After Sampling At Toiyabe And East Saddle; Recently Raised C$1.66M In Oversubscribed Non-Brokered PP

With the gold price holding strong above US$2,300/oz levels, perhaps due to the Russia and Israel conflicts aggravating while inflation increases again - thus delaying timing of upcoming rate cuts by the Fed – Westward Gold Inc. (WG.CSE) is progressing on the exploration front and recently announced positive sampling results for Toiyabe and East Saddle, after raising an oversubscribed and non-brokered sum of C$1.66M last month. This amount is impressive for a tiny C$9.3M market cap company, and will support Westward with advanced drill-targeting, potential M&A and general working capital during 2024. As I have been hearing CFO Andrew Nelson talk about potential M&A in order to grow the market cap to more meaningful size and attract more capital for quite some time now, it was time to ask some in-depth questions, giving him the opportunity to explain the current state of affairs, and ongoing strategy at Toiyabe.

All pictures are company material, unless stated otherwise.

All currencies are in US Dollars, unless stated otherwise.

Please note: the views, opinions, estimates, forecasts or predictions regarding Westward Gold’s resource potential are those of the author alone and do not represent views, opinions, estimates, forecasts or predictions of Westward or Westward’s management. Westward Gold has not in any way endorsed the views, opinions, estimates, forecasts or predictions provided by the author.

Although Westward already completed meaningful drilling at Toiyabe, a large part of their consolidated 40km2 land package remained underexplored, so the company is in the process of sampling all claims.

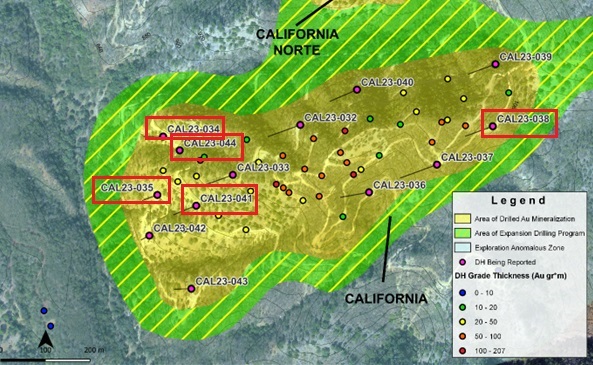

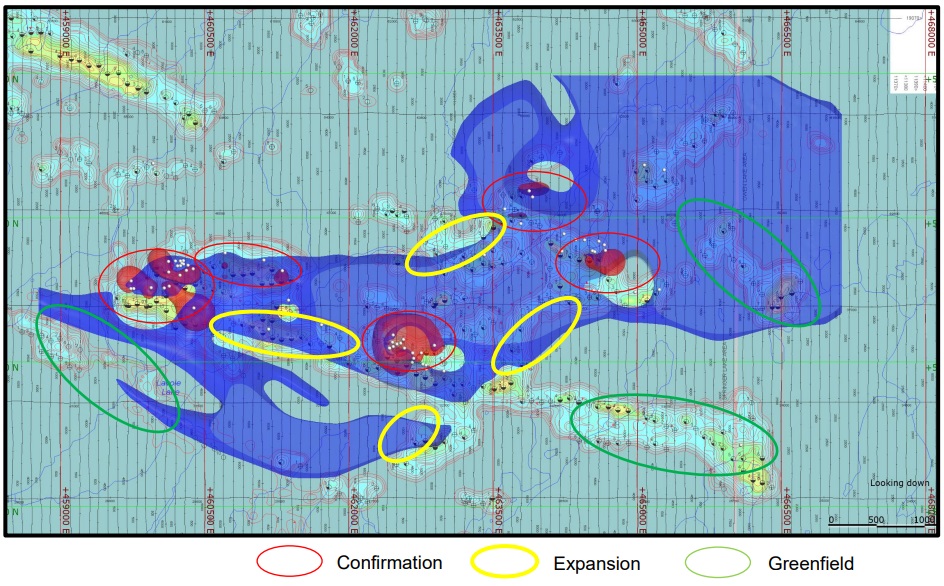

Recently announced results were part of the 2023 winter program, and Westward has recently commenced new exploration activities for this year, after the inevitable winter break. The 2023 program sampled for gold in soils, rock chip gold samples, arsenic in soils and antimony in soils, maps below indicating different highlighted zones for each (from left to right gold, arsenic and antimony):

The gold sampling for Toiyabe showed lots of robust gold grade samples, plus East Saddle indicated a new trend, including the entire 5km long strike length of the Roberts Mountains Trust (RMT) Fault at East Saddle. There seems to be a lot going on in the southwest portion of the land package, thinning out to the northeast. This was confirmed by Strategic Advisor Kelly Cluer:

“The general geology indicates that major strata of the lower and upper plates dip gently to the east in the area of the new soil array. This indicates that significant portions of the large geochemical footprint are preserved under relatively shallow cover, and coincide with major geophysically-imaged structural corridors – an ideal setting for new discoveries.”

As the gold sample results for Toiyabe indicated lots of high-grade gold (magenta triangles represent 0.25-16.5ppm Au or g/t Au which is very good, as 20ppb Au is already considered interesting enough to warrant follow-up exploration), I consider this the most important target zone. CFO Andrew Nelson had this to say about this assumption: “With our historical resource at Toiyabe and the mined-out Toiyabe Saddle pits, there is a gold endowment already of ~300,000 ounces from historical production and our historical resource. This is the smoke, now is time to find the larger source of this gold mineralization in the lower plate which is what we’re currently tasked with. The rock chips, soils, and additional geophysics will help with this greatly.”

The arsenic sampling indicated a huge concentration immediately to the east of historical mining operations at the Toiyabe-Saddle open pits. Arsenic is a key pathfinder element for Carlin-type gold deposits in this geological setting. According to VP Ex Robert Edie, arsenic-in-soil values decrease to the east, likely indicative of a gradual eastward thickening of upper-plate lithologies that effectively attenuate geochemical signals. Despite this directional weakening however, the anomalous arsenic feature is apparent over 5+ km and remains open to the east, which speaks to its scale.

The antimony sampling indicated a large anomaly in the south of East Saddle. As antimony also serves as an important gold indicator, I asked Mr. Edie why the location of the antimony anomaly clearly differs from the arsenic anomaly, and how he is interpreting this. VP Ex Edie answered: Antimony is less mobile than arsenic in a Carlin-type depositional setting. The eastward trend grading from strong arsenic into strong antimony gives us a likely exploration vector towards gold.

After discussing these exploration results, let’s have a look at the recently completed financing. It was good to see Westward increasing the financing from the initially announced C$1M on February 28, 2024 to C$1.5M on March 6, 2024 to finally C$1.66M on April 5, 2024. The financing was non-brokered as mentioned, done at 8c with a full 2-year warrant (exercise price 12c), adding 20.8M shares and an equal number in warrants. A finders fee of C$25k in cash and 342k finders warrants were issued as well. Management didn’t shy away from participating together with certain insiders, acquiring a total of 2.85M shares. As the structure had 95.8M shares, quite a bit of dilution is added when fully diluted (total of 189M F/D), but that is the necessary path of every junior explorer with no income. With the financing done in August of last year, upper management of First Majestic and the likes of Terry Salman came in. This time they had major support from Haywood Securities with some of the biggest brokers there participating.

On a sidenote, Westward also managed to acquire the last part of their flagship Toiyabe project in Nevada under the earn-in with Minquest, by completing a final share-based payment of C$318k on February 20, 2024. It’s entire land position is now 100% owned by the company.

As a reminder, after closing an oversubscribed non-brokered C$1M financing in August 2023, the proceeds of this particular financing were designed to a) follow-up work from the recent diamond drilling at its flagship Toiyabe Project (about C$500k), b) for general working capital purposes, including upcoming annual BLM claim maintenance fees (C$125k), and especially c) to advance potential accretive M&A opportunities (about C$400k) in order to grow market cap, thus being able to attract more capital. Alongside this, management has been busy to explore creative strategies to fund further drilling (ie. strategic investment from a major, exploration partnership, or potential JV if the terms are right).

Since no M&A or other creative strategies was announced since last year’s financing, I wondered what was going on in this department, as reportedly deals were imminent in November and December of 2023.

CFO Andrew Nelson elaborated as extensively as he could: “We have been very active on the M&A front, behind the scenes, having discussions with counterparties and even submitting offers. We were at the table bidding for Contact Gold in Q1 but couldn’t compete with the $1.7B market cap of Orla Mining who was the successful bidder. We also thought Timberline Resources was interesting but McEwen Mining beat us to the punch. Both of those companies had something we are actively looking for, sizable gold deposits we believed had significant room for growth, but those were also sought after by mid-tier producers Orla Mining and McEwen Mining. We are continuing to discuss with other companies for assets and seek out additional advanced projects to bring into our portfolio, but these negotiations always take longer than expected.”

Fortunately, this didn’t hold Westward back in the exploration department, as it has completed various sampling and mapping programs in Q4, 2023. As a reminder, Carlin expert and Technical Advisor Steven Koehler thinks Toiyabe could be hosting a significant deposit, as he noticed several similarities with the early-stage discovery of the multi-million-ounce Cortez Hills and Leeville deposits. According to him, there is mounting evidence that Westward’s exploration ground contains many of the same key geological features that were identified at the nearby Cortez Hills Mine during its early-stage exploration (now operated by Nevada Gold Mines). These include dike-filled fault corridors, multiple compressional tectonic events, shallow gold mineralization in tandem with a second deeper zone (both open in several directions), and multiple horizons of favourable carbonate host rocks.

Notably, Steven Koehler has been instrumental in the Company’s understanding of this important analogue, having been on the initial discovery team at Cortez Hills in the early 2000s. He thinks the hydrothermally altered SSD Zone extends and strengthens to the northeast, and this is where further drilling will focus, preferably widely-spaced step-out drilling, for which permits are already in hand. Koehler commented further:

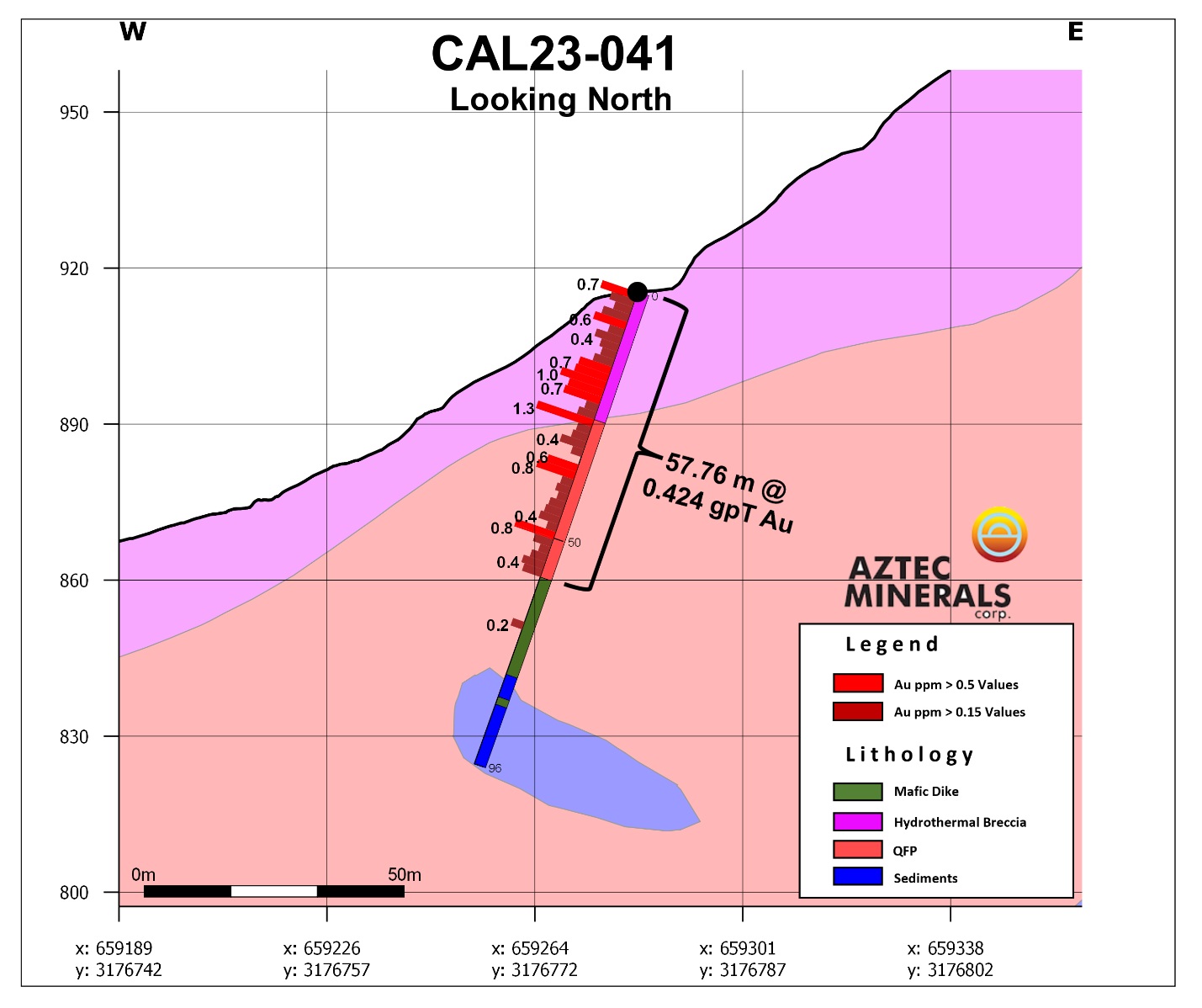

“Hole T2301 confirmed that the gold system remains open downdip to the north and east, and that gold mineralization encountered in legacy drilling is hosted in upper plate siliciclastic rocks and lower plate carbonate rocks – an attribute that was poorly-understood historically. Upper plate gold occurrences along major Nevada gold trends typically form above, or proximal to, larger lower plate carbonate hosted Carlin-type gold deposits. T2301 is reminiscent of geologic patterns in the Carlin Trend north area – especially those gold deposits down-dip from the Carlin and Pete open pit deposits.”

Lots of step-out drilling needs to be completed to establish the stratigraphy here. It also needs to be noted that existing large deposits (owned by the likes of Barrick and NGM) start around 200-550m below surface, and extend to 1,200m of depth as mentioned. NGM seems to be on the same kind of exploration track with the Swift Project of Ridgeline Minerals, committing to a US$30M earn-in after some results that were hardly comparable to the ones Westward generated recently. As Toiyabe seems to have the same features, Westward management isn’t done exploring yet.

Additional field programs have been designed to further Westward’s understanding of the consolidated Toiyabe district as a whole. This includes the Company’s Toiyabe, Turquoise Canyon and East Saddle Projects, with approximately 40 square kilometres of fully-contiguous exploration ground between the 3 projects. At Toiyabe, a systematic relogging of all available legacy RC and core drillholes (~15,000 meters total) is ongoing. Re-logging of the historic drill core is further fine-tuning Westwards geological model at Toiyabe to increase the probabilities of a future discovery at their 100%-owned district scale land package.

Rob Edie, Vice President of Exploration at Westward Gold’s core shack in Crescent Valley, Nevada

The program aims to correlate stratigraphic, structural, and alteration features identified in T2301 with gold mineralization, improve upon historical interpretations based on Westward’s recent findings, and standardize datasets with more thorough and detailed observations. A new set of cross-sections will be created and analyzed, in addition to surface rock sampling and soil sampling, in order to identify new target opportunities on the property, and refine the geological model at Toiyabe.

After lots of samples were collected, VP Ex Robert Edie was excited: “After completing my first significant stint in the field since joining the Company, I’m delighted to confirm with my own eyes that the Toiyabe Properties and Coyote/Rossi contain several key components necessary to host Carlin-type gold deposits. Compressional tectonics, hydrothermal alteration, and the presence of igneous dikes were all verified. The important puzzle pieces are there and the process of putting them all together is well underway.”

After completing the field program, Robert Edie found more evidence of the geological concept they are pursuing:

“I’m very pleased to have discovered an array of specimens on the property which exhibit features consistent with Carlin-type gold deposition. Strong, surface-level oxidation is an important characteristic of these deposits and relates to the abundance of pyrite formed, a key component of gold-hosting systems. Tectonic breccia speaks to the structural preparation of host rocks; the gold-bearing Carlin fluid uses these structural pathways to rise from depth where it interacts with the meteoric water table and geochemically precipitates gold – preferentially into carbonate rocks.”

Mr. Edie had this to say about the East Saddle Project:

“Decalcification and silicification of carbonate rocks is a distinct marker of Carlin-type gold deposition. It occurs when gold-bearing Carlin fluid dissolves calcium carbonate from limestone host rocks and deposits silica pervasively. In addition to silica, the process also deposits gold and other pathfinder elements. The discovery of decalcified, silicified limestone at East Saddle suggests that the area has experienced a Carlin-type mineralizing event.”

This all looks good for follow-up recon exploration, and is understandable as deep drilling would cost a small fortune. However, I am intrigued by the reasoning behind all the surface exploration, after deep hole T2301 hit mineralization, and the sought after mineralized deposits typically reside at depth, following the established concept:

One would think that the company just should continue drilling at this point. Why were Westward geologists returning to sampling again, following the sequence surface – drilling – surface? The geologists were already Nevada Carlin experts, before Mr. Edie came in. It could look a bit like the company could have done more surface exploration before vectoring in at depth by drilling, or T2301 might have been just to establish geology/stratigraphy, and they got lucky in a sense by hitting mineralization. CFO Andrew Nelson had the following extensive explanation: With Kelly Cluer, former Senior Director of Global GeoScience at Kinross Gold joining us in late January 2024, he wanted us to have 5-10 reasons to drill a target, not 1 or 2 reasons. By layering multiple data sets on a drill target, we can prioritize and go after our highest probability drill targets to give our shareholders the best shot at success. We are currently underway with our 2024 exploration program, conducting multiple pre-drilling programs to collect as much new data to build the most compelling set of drill targets to test in the near future.

Conclusion

New VP Exploration Robert Edie didn’t sit on his hands when coming in and has been busy from September 2023 to January 2024 with lots of sampling and mapping, interpreting results, and compiling all information. The results of all hard work look promising, and after raising an oversubscribed C$1.66M Westward is ready to embark on further programs this summer. With this data in hand, Westward management will be able to select and promote fresh and exciting drill targets. If sampling results and other exploration generates enough confidence to go to the markets again and raise more, hopefully riding positive gold sentiment from now on, drilling at Toiyabe could start in Q3/Q4 of this year depending on capital availability. Stay tuned!

I hope you will find this article interesting and useful, and will have further interest in my upcoming articles on mining. To never miss a thing, please subscribe to my free newsletter at www.criticalinvestor.eu, in order to get an email notice of my new articles soon after they are published.

Disclaimer:

The author is not a registered investment advisor, and currently has a long position in this stock. Westward Gold is a sponsoring company. All facts are to be checked by the reader. For more information go to www.westwardgold.com and read the company’s profile and official documents on www.sedar.com, also for important risk disclosures. This article is provided for information purposes only, and is not intended to be investment advice of any kind, and all readers are encouraged to do their own due diligence, and talk to their own licensed investment advisors prior to making any investment decisions.