An Interview With Dolly Varden Silver CEO Shawn Khunkhun And VP Ex Rob Van Egmond

After hitting impressive intercepts like 25m @ 46,3g/t Au at Homestake Ridge and 15,94m @ 1499g/t Ag at the Wolf Vein, Dolly Varden Silver (DV.V)(DOLLF.US) seems to have taken the main stage of successful exploring juniors.

Beside the headline-grabbing results, this has also a lot to do with the increasing tonnage potential because of these stellar results, as beforehand years of drilling under different management didn’t seem to make much of an impact, since the resource barely increased. With CEO Shawn Khunkhun and VP Exploration Rob Van Egmond at the helm, a different wind seems to be blowing now, as Khunkhun has raised the bar much higher by attracting more capital, and doing deals like buying Homestake from Fury, and Van Egmond doing his magic in exploration, bringing home much better results.

Of course, with exploration there is luck involved, but considering progress things are clearly shifting now. As such it is very much time to discuss the latest batches of results, exploration strategy, goals and expectations and much more, so I sat down with both men for an interesting interview.

All pictures are company material, unless stated otherwise.

All currencies are in US Dollars, unless stated otherwise.

Please note: the views, opinions, estimates, forecasts or predictions regarding Dolly Varden Silver's NPV and resource potential are those of the author alone and do not represent views, opinions, estimates, forecasts or predictions of Dolly Varden Silver or Dolly Varden Silver's management. Dolly Varden Silver has not in any way endorsed the views, opinions, estimates, forecasts or predictions provided by the author.

The Critical Investor (TCI): Welcome guys, good to see you both had some spare time in this very busy period.

Shawn Khunkhun (SK): Thank you, grateful for the opportunity. It is a pleasure to be here talking to you.

Rob van Egmond (RE): Yes, thank you for taking the time to talk to us.

TCI: Let’s start with some macro first, before we focus on things like financials and drill results. With the Fed hesitating what to do regarding rate hikes, inflation not slowing down and stock markets in risk-off mode, with many expecting a recession on its way and precious metals not performing as convincingly as many expected in a high inflation environment, what do you think we can expect on a macro economic level and why, and what impact could this have on precious metals and why? I’ll probably leave that for you Shawn to answer.

SK: Why are central banks are record buying more gold than in any other time in history? I believe that with inflationary pressures, rising and record high debt levels, gold will protect from the erosion of loss of purchasing power. Regardless of the macro theme, there is a shortage of new mineral inventory in the precious metals space. New resources in the ground, that are high-grade and in mineable jurisdiction are highly valuable.

TCI: Interesting. It sounds more and more you raised that C$22.6M flow through at the right moment at the end of December last year, it must be nice to have such powerful backers like Eventus. I noticed that Hecla participated again. Do you have any idea what their agenda is? They could buy Dolly Varden many times and much cheaper, but failed.

SK: We are grateful to all of our investors, retail, Eric Sprott, the institutions. Hecla is unique in that they are a corporate that produces the metal and in the last 12 months have acquired 2 projects in Canada. I think Phil Baker, their CEO has done a tremendous job at the helm and we are accepting of both their technical and financial support.

TCI: It is good to see a full treasury in these days of increasing turmoil. What is your burnrate per quarter on average, and how long do you anticipate these funds will last?

RE: It changes during exploration stage from May to October is will be about C$3.5M per month while drilling.

SK: With over C$26M in the bank we are in a strong position. Our burn rate fluctuates at our discretion. Our goal this year is to put over $20M in the ground.

TCI: Investors apparently appreciate what you guys are doing, as the share price shows a solid leg up since heavy selling in September halved the stock in barely 2 weeks.

Share price 10 year time frame (Source tmxmoney.com)

As the chart indicates, we are very close or might have even overtaken the 2020 highs a few weeks ago, meaning we have to look back all the way up to 2014 to see higher prices. Back then it was a full-on bear market raging, as the stock came from 2 dollars at the highs. What is the strategy you have in mind Shawn, are you looking at organic growth now, raising money at higher prices, growing the resources to what levels? Looking for further consolidation or take it easy and is it a matter of resource growth now after the acquisition?

SK: If it isn’t broke don’t fix it. I took over in February 2020 at $0.245/share and have raised about $65 million at an average price of over $.80. We have significantly grown the resource with almost 50 million silver equivalent ounces indicated and almost another 90 million ounces inferred. We have successfully built a world class team that has made discoveries, growing beyond the known resources. We have successfully minimized dilution with well-timed and strategic financings. Moving forward we will continue to look to grow through exploration and regional consolidation.

TCI: I always wondered why you didn’t take over Strikepoint, which has no business developing their Porter project as a standalone, as it simply needs a party like Dolly Varden which can integrate the project into something larger.

SK: Our next chapter is organic growth with the newly acquired Homestake Ridge ground that is continuous and to the North. That will be our focus for growth.

TCI: When discussing share prices, there is another interesting feature that we should mention, and this is the upcoming rebalancing of the SILJ ETF, coming at the end of March. Do you guys think this could have an impact?

SK: The last rebalancing of the ETF on December 16, 2022 had a materially impact on Dolly’s share price, as the $700 million ETF increased its stake from .03 to .055. With Yamana being acquired and being a 10% holding of the ETF, those funds need to be rebalanced. Dolly potentially may be a benefactor.

TCI: As your cash position stands at C$22M at the moment, you are sufficiently cashed up for the rest of the year?

RE: Yes, of the C$28M in cash we had about a month ago, we need to spend C$20.7M flow through money this year, and we need to work hard to get to this as we have a winter break. The plan is to drill 40,000-50,000m.

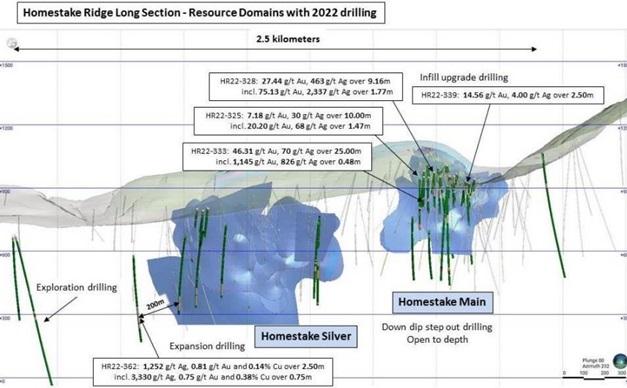

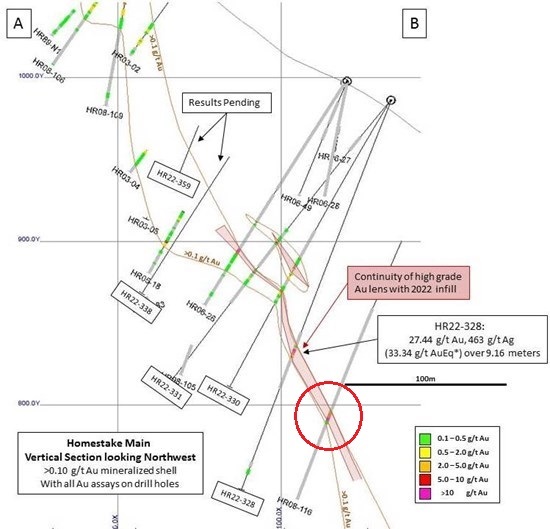

TCI: Let’s discuss the excellent drill highlights from the 2022 program that came in during January and February. Obviously HR22-035 was an eyecatcher with 25m @ 46.3g/t Au at Homestake Ridge, when looking at the sections and map it seems more of an infill hole at Homestake Main?

RE: Yes this is correct, the program was designed for 50% infill/upgrading and expansion, and 50% step-out exploration. For the upgrading the grid spacing had to go from 50m to 25m. The upgrading was focused on the higher grade ounces, and so far everything is going according to plan. Our geology model is confirmed by using oriented core.

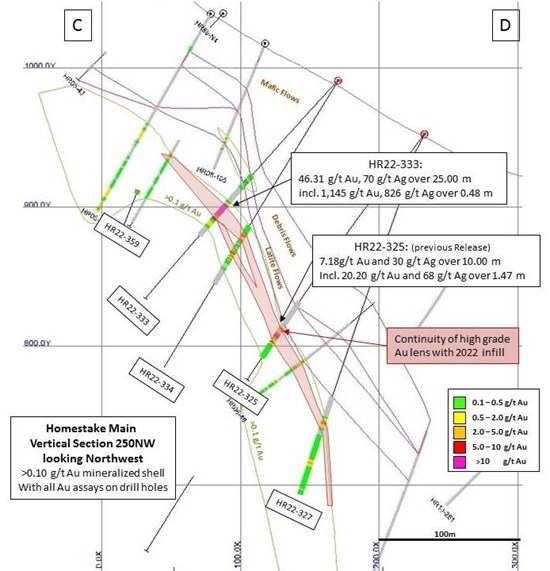

TCI: HR22-038 was very good too with 9.16m @ 27.4g/t Au, when looking at the sections there is a historic drillhole on strike: HR08-116.

I couldn’t find the drill result in the NI43-101 report, do you happen to know this by any chance?

RE: I do not have those numbers on hand, they are in our database, but if you look at the color code in the legend you can get an idea of individual samples

TCI: I also noticed there were 3 holes at the Homestake trend that hit nothing, would you like to continue there and why?

RE:A sediment cap blocked geological concept interpretation as we couldn’t see any alteration, increased potassium etc from surface by mapping and geophysics. I had a theory about projecting potential mineralization under the cap, so we drilled a few wildcat geological holes to test this, but it didn’t work out unfortunately. In the upcoming program there we are planning closer step-out holes. We did hit on a 200m step out south of Homestake Silver, so another less aggressive step out south will be done.

We also found there were lots of gold in soils, and we need to explore this further to explain. Another important indicator for gold is the presence of rhyolite domes, like with Eskay Creek.

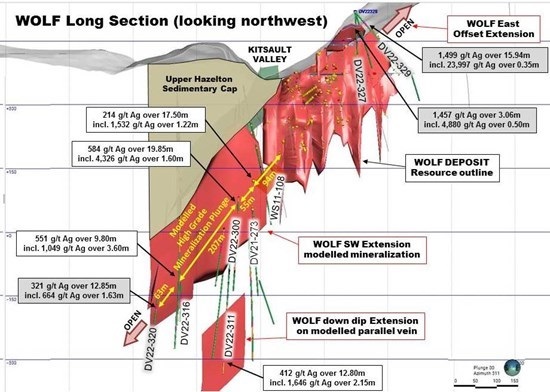

TCI: That wraps it up for the gold, let’s talk silver now. The 15,94m @ 1,499g/t Ag Wolf Vein intercept including 0.35m @ 23,997g/t Ag was truly something special, with a residual grade of 993g/t Ag which is still very high. Further step-outs and other results extended the Wolf Vein at depth, narrowed it down but also identified an off-set parallel vein:

I noticed despite the ultra high grade intercept, most intervals were low grade, did you expect this extreme variation here, and does it change your strategy now at the Wolf Vein?

RE: No, it does not change our strategy, we are infill drilling the 200m step-outs to 70-75m, and keep focusing on the extension at depth.

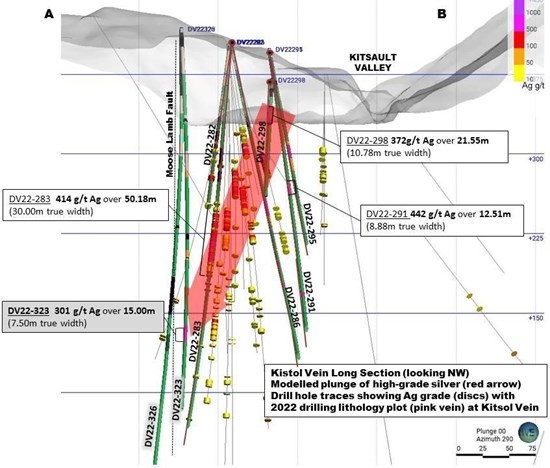

TCI: The Kitsol Vein is also shaping up to be a nice, pretty narrow but very continuously mineralized expansion, as can be seen here:

The average grade is fairly consistent (around 350g/t Ag on average) in a steeply plunging high grade vein in the center of the extension down dip, surrounded by a low grade halo. Hole 326 seem to have missed this vein, do you believe it has ended?

RE: Hole 326 is the western most hole and crossed a fault that has cut across the vein. On the other side of the fault the vein has been offset. We will be targeting where we believe that continuation might have been shifted to this summer.

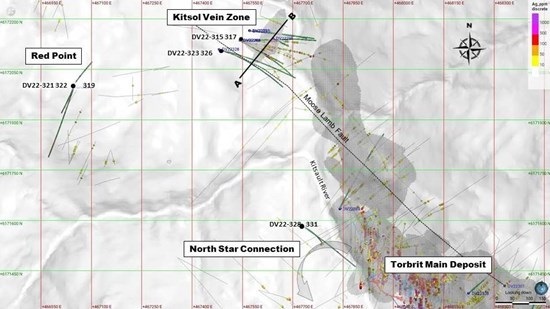

TCI: As Dolly Varden is also testing a step-out target 500m to the west of the Kitsol Vein, called Red Point, it was good to see them hitting several gold intercepts, with the following results of the two drill holes:

- DV22-321: 0.59 g/t Au over 49.00 m

- DV22-321: 2.94 g/t Au and 1.65% Cu over 5.00 m

- DV22-321: 8.10 g/t Au, 244 g/t Ag and 5.16% Cu over 1.00 m

- DV22-322: 17.20 g/t Au and 1.93% Cu over 1.15 m

As that target already has seen quite a bit of historic drilling, as can be seen at the map, I wondered if management is using a different approach this time for Red Point.

RE: We have completed ground geophysics over the area in 2022 that has given us a better target horizon. This season we will be following up in the area and doing the same geophysics to the north.

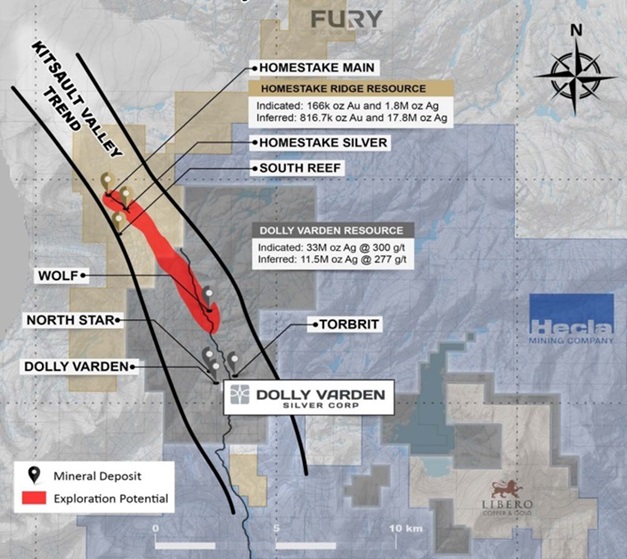

TCI: The objective of drilling during 2022 at the Homestake Main and Homestake Silver deposits was to expand multiple, subparallel mineralized zones and to upgrade Inferred Resources in areas where the current model shows the thickest and highest grades. Once higher grade ore shoots were defined, the down plunge extensions were tested for continuity to depth. Dolly Varden completed a total of 56 drill holes for 18,448m of drilling at Homestake Ridge, and a total of 52 holes for 18,614m at Dolly Varden during 2022, making for a grand total of 108 holes for 37,062m last year.

As a reminder, the 2019 NI43-101 compliant resource estimate for Dolly Varden stands at 32.9Moz @ 299.8g/t Ag Indicated and 11.4Moz at 277g/t Ag Inferred. Homestake Ridge’s 2022 NI43-101 compliant resources includes 0.16Moz gold with 1.8Moz silver Indicated and 0.81Moz gold with 17.8Moz silver Inferred.

For Torbrit I assumed a 300x150x8x2.75 = 990kt envelope, containing 9.6Moz Ag at an average estimated grade of 300g/t Ag, which is slightly more than my earlier estimate of 7.4Moz @ 280g/t Ag. For the Wolf Vein, which has a more erratic grade distribution, it would be an estimated 450x140x4x2.75=693kt, at an average estimated grade of 350g/t Ag this results into 7.8Moz Ag. The Kitsol Vein is considerably smaller, but still an estimated 180x50x10x2.75x350g/t = 2.8Moz Ag.

All in all, including the infill drilling which found much higher grades in some instances, I do believe Dolly Varden might have added another 22-24Moz Ag after 2022 drilling, which could mean an estimated increase of 30-40% of their silver resources. I asked VP Van Egmond if my ballpark numbers could be realistic.

RE: Yes, I do believe we are heading this way, also with the average grades for Torbrit and Wolf, although the total average will likely be closer to 300g/t again.

TCI: Could you tell us more about the upcoming drill programs for Kitsault Valley?

RE: These programs will start around the first week of May, 2023, with 4 drill rigs in operation by the end of May, with a focus on Homestake Ridge exploration expansion and exploration for discovery of additional mineralization at Dolly Varden. Due to the discovery success at Wolf and other exploration targets in 2023, the focus will shift to seeing how large this system is and infilling the new discoveries to get them into the next resource update. Current large step out spacing at Wolf is too wide for even Inferred Resource classification, but will be infilled to 70-75m as discussed. We will start at Wolf, and will drill up to 700m depth. We will start at Homestake in the beginning of July, due to a fairly long winter break in the area although it hasn’t snowed as much as usual.

TCI: Could you elaborate on future resource estimates and economic studies?

RE: Sure, an updated Mineral Resource estimate for the combined project is planned for Q2 of 2024, and will be used in a consolidated PEA for the Kitsault Valley project, which is scheduled for H2, 2024. This seems long, but we prefer to see what the maximum potential could be at Kitsault Valley, plus in terms of material change reporting this would only be the case when there is a resource increase of at least a 100%.

TCI: Thanks Rob, that makes sense. I believe we have discussed the most important subjects of Dolly Varden by now, do you have anything you could add as a closing statement Shawn?

SK: There is so much information to close with, I guess the key is Dolly Varden is a leading take over candidate. We are where size meets grade in a safe jurisdiction. Our differentiator is that it is the only project with this level of resources in terms of size of both silver and gold at these grades in the US or Canada.

TCI: That sums it up nicely. Thank you guys for your time, and I’m looking forward to the next batches of drill results, and see where this could lead us in terms of resource potential, and in turn economic potential.

As a reminder, I estimated a Kitsault Valley after-tax NPV5 of US$300M to be within reach (= C$380M) at US$1620/oz gold and US$14.40/oz silver. At current precious metals prices this could even increase to an estimated C$610M-650M, and even further past C$750-850M when drilling continues to be successful and we could see the projected resource target becoming a reality. It will take a while before the consolidated PEA comes out, and it usually is discounted because of the high margin for error, but the future potential for Dolly Varden, with a current market cap of C$243M is significant for sure.

Conclusion

After completing their 2022 drill program last December, Dolly Varden Silver received pretty impressive drill results. According to my estimates, besides likely bringing a significant part to higher categories up from Inferred, gold resources could have grown by 300-400koz Au, and silver resources by an estimated 22-24Moz Ag, which is considerable and a 40-60% increase. As management indicated, they aren’t looking to come out with a resource update below a 100% increase, so this makes their timing of Q2 2024 realistic. With the last raise of C$22.6M Dolly Varden is set for drilling all year, and I’m looking forward to further strong results for ongoing derisking and expansion. Stay tuned!

I hope you will find this article interesting and useful, and will have further interest in my upcoming articles on mining. To never miss a thing, please subscribe to my free newsletter at www.criticalinvestor.eu, in order to get an email notice of my new articles soon after they are published.

Disclaimer:

The author is not a registered investment advisor, and currently has a long position in this stock. Dolly Varden Silver is a sponsoring company. All facts are to be checked by the reader. For more information go to www.dollyvardensilver.com and read the company’s profile and official documents on www.sedar.com, also for important risk disclosures. This article is provided for information purposes only, and is not intended to be investment advice of any kind, and all readers are encouraged to do their own due diligence, and talk to their own licensed investment advisors prior to making any investment decisions.

Dolly Varden district

This newsletter/article is not meant to be investment advice, as Criticalinvestor.eu (from now on website, newsletter, and all persons or organisations directly related to it, for example but not limited to: owner, editor, the Seekingalpha author The Critical Investor, publisher, host company, employees, associates, sponsoring companies) is no registered investment advisor. Therefore it is not intended to meet your specific individual investment needs and it is not tailored to your personal financial situation. This newsletter/article reflects the personal and therefore subjective views and opinions of Criticalinvestor.eu and nothing else. The information herein may not be complete, up to date or correct. This newsletter/article is provided in good faith but without any legal responsibility or obligation to provide future updates.

Through use of this website and its newsletter viewing or using you agree to hold Criticalinvestor.eu harmless and to completely release them from any and all liability due to any and all loss (monetary or otherwise), damage (monetary or otherwise), or injury (monetary or otherwise) that you may incur.

You understand that Criticalinvestor.eu could be an investor and/or active trader, meaning that Criticalinvestor.eu could buy and sell certain securities at all times, more specific any or all of the stocks mentioned in own newsletters/articles and other own content like the Watchlist, Leveraged List, etc.

No part of this newsletter/article may be reproduced, copied, emailed, faxed, or distributed (in any form) without the express written permission of Criticalinvestor.eu. Everything contained herein is subject to international copyright protection. The full disclaimer can be found here.