Platinex Going To Joint Venture Shining Tree With Fancamp Exploration; Raises C$2.5M

After acquiring the Muskrat Dam Critical Minerals project in Ontario, with a focus on the extremely hot metal lithium, it was good to see Platinex (PTX:CSE)(9PX:FRA) bringing in Fancamp Exploration (FNC.V) as a partner for the Shining Tree gold project in the same state, as it had 3 district-scale exploration projects in its portfolio by then, which is a bit much for the average C$8-10M market cap. As part of the deal, Fancamp will transfer their Heenan Mallard and Dorothy gold projects into the JV Goldco for 25% of shares in Goldco, Platinex will own 75% of Goldco by virtue of maintaining their Shining Tree project in Goldco (which it previously owned 100%), and Platinex will conduct a private placement for C$2.5M, of which Fancamp will take up 9.5% of outstanding Platinex shares.

All pictures are company material, unless stated otherwise.

All currencies are in US Dollars, unless stated otherwise.

This is an interesting deal, as Platinex needed cash for exploration of three large projects, and Fancamp has lots of cash. As Platinex CEO Greg Ferron is also a director of Fancamp, it probably didn’t take long to figure out a way to both benefit Platinex and Fancamp, as Fancamp is looking to downsize their huge portfolio of assets, and put its cash pile to work and both projects are located in the same camp along the prolific Rideout Tyrell Deformation Zone (RDZ) which host numerous gold deposits such as Borden Mine, Cote Gold and Juby Deposit. The agreement was announced on February 6, 2023, and CEO Ferron was happy about it:

"The transaction achieves a number of goals for Platinex. It creates a stronger gold-focused growth vehicle in a world class Ontario gold camp and brings in a strong joint venture partner, Fancamp with access to capital and technical expertise, allowing us to accelerate exploration at Shining Tree Gold Project. The newly acquired Heenan Mallard Gold project which borders IAMGOLD’s Côté Gold Project, and the Shining Tree Gold Property are expected to be the first projects to be drilled. The transaction provides a clear strategy for the enhanced gold portfolio while retaining a 100% ownership of our high-quality W2 Ni-Cu project and the recently acquired Muskrat Dam Critical Minerals Project."

As Platinex will be the operator until Fancamp exercises its option to acquire another 25%, and has no shortage of its own geological expertise in the region, it is clear for me that the main reason was the capital Fancamp was willing to invest here. Besides the 25% ownership in Goldco, Fancamp will also be granted a 1% NSR royalty on the Heenan Mallard gold properties, which will decrease to 0.5% when Fancamp elects to exercise its option for 50% ownership.

Here are additional terms of the JV agreement:

- The board of Goldco will consist of three directors in respect of which Platinex will have the right to appoint two directors and Fancamp the right to appoint one director

- Fancamp shall have the right to nominate one director to the board of directors of Platinex, which right shall remain subject to Fancamp holding not less than 7.5% of the issued and outstanding shares of Platinex, calculated on a non-diluted basis.

- A management/technical committee (the "Technical Committee") of Goldco will be created in respect of which Platinex will have the right to appoint two members and Fancamp the right to appoint one member

- Goldco will engage in an initial exploration program of C$1.1million (the "Initial Exploration Program") to be funded by the Platinex Financings (as described below) and an additional sum of $130,000 to be advanced to Goldco by Fancamp. Platinex shall contribute a minimum of $940,000 to Goldco in respect of Goldco’s operation.

- Within 60 days from the completion of the Initial Exploration Program, Platinex as Operator shall prepare an exploration program (the "Phase II Exploration Program") to be approved by all of the members of the Technical Committee and the board of Goldco

- Fancamp will have the right and option (the "Option") to increase its ownership interest in Goldco to own up to 50%, which may be exercised over a two-year period commencing on the date of approval of a Phase II Exploration Program by making staged cash payments to Goldco in the aggregate amount of C$1,500,000 to be used for exploration activities of Goldco

As I assume the Phase I exploration program including the 60 days period will take up to one year, the additional two-year period will make for a hypothetical three-year period of operator time for Platinex, and basically predominantly funded by Fancamp this way. This seems like a good deal for Platinex, as it wouldn’t cost them much capital to raise, and with C$2.5M one could do decent drilling and further exploration.

In addition to the JV agreement with Fancamp, Platinex intends to raise cash through a non-brokered private placement, raising up to C$1.5M @ 4c (0.055c 5y half warrant), and a non-brokered flow-through private placement for up to C$1M @ 0.045c (also a 0.055c 5y half warrant). Both warrants are subject to an acceleration clause, triggered when Platinex is trading over C$0.15 for 20 consecutive trading days. Both financings are subject to a hold period of 4 months and one day. At first glance FT shares priced at 4.5c seemed very cheap considering the tax advantages of FT, as the stock traded at this price at the time of announcement, so I asked CEO Ferron why he didn’t price it at a robust premium, as is standard. He answered that the hard dollar financing was based on the CSE requirements for shares below 5 cents - based on a minimum 20 day VWAP at the time of pricing which was negotiated and agreed on a few weeks prior to announcement. Ontario gold flow through premium (not charity structure) generally receive a modest premium to the hard dollar price which was also at a decent premium to the market at the time. I also wondered what part of FT and non-FT Fancamp was taking up, to which he replied: “I can’t disclose anything more than as part of the transaction they will acquire an position equivalent to approximately 9.5% of the company’s issued shares upon closing the placement.” As the current market cap hovers around C$8-10M, this would account for about C$850k-1.5M after closing.

The transaction is expected to close on or about February 24, 2023, or on such other date and time as is mutually agreed to between Platinex and Fancamp.

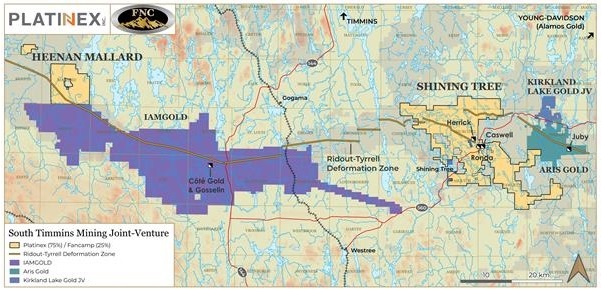

Let’s have a quick look at the properties Fancamp put into the JV Goldco. The most important project is the Heenan Mallard gold project, and is located on the Ridout Deformation Zone bordering Iamgold’s Côté Gold claim package and is approximately 25 km west of the soon to be producing Côté Gold mine.

When looking at this map, Shining Tree expanded further to the west of Ronda this time, and one could easily start to think of substantial parts of the Ridout-Tyrell Deformation Zone waiting to be consolidated, with Juby being of interest as a cornerstone asset here. CEO Ferron had this to comment on this subject: “With IamGold’s Cote going into production in 2024 and having several other producers in the camp I anticipate that further investment and consolidation will occur in the Shining Tree camp in the future. The South Timmins JV now has two assets, one in Shining Tree and one nearby Cote Gold.” Historic drilling of a modest 14 holes by Noranda in 1985 returned several modest high-grade near-surface intercepts, including 5.04 g/t Au over 3.69 m core length (BE-85-1), 5.31 g/t Au over 3.82 m core length (BE-85-6), 3.50 g/t Au over 2.80 m core length and 6.62 g/t Au over 1.82 m core length (BE-85-3). The big difference with the eighties is there is a nearby mine and mill these days.

Prospecting, geological mapping, soil sampling, and geophysical surveys carried out by Fancamp at Heenan Mallard in 2019-2020 have generated multiple targets in other sections of the project. Of these, the two most highest priority gold targets identified currently for follow up drilling are an undrilled gold showing at Heenan that is coincident with an IP anomaly and an undrilled zone along the Ridout shear at Mallard with a coincident soil and IP anomalies. The second project is the Dorothy gold project, which is grassroots and doesn’t provide much data yet, and located adjacent to Dynasty’s Thundercloud gold discovery. Although I didn’t immediately see potential synergies by adding Heenan Mallard to Shining Tree as both are 60km apart, it should have qualities. CEO Ferron explained why: “I like the idea of increasing discovery and resources potential with two assets in the same camp that will be consolidated and decrease risk for shareholders. Both projects are on the underexplored RDZ which hosts major deposits. The Platinex technical team is in place and same crew will work both projects and same drilling rig etc. We have knowledge of the asset in house (Jim Trusler and Blaine Webster) and Fancamp will be on the technical committee.”

Chairman Trusler and Technical advisor Webster were also happy to elaborate on the advantages of Heenan Mallard:

Trusler: “For Heenan Mallard the Mallard portion provides several high hit probability opportunities. The River and Camp zones were previously drilled by Noranda in a limited program, never followed up, which obtained four potentially commercial intersections with a best value of 5.04g/tAu/3.7m. A recent IP survey has revealed additional targets here. The 1.1 km wide Ridout deformation Zone, covers 5-6km of strike length on the Mallard property. Fancamp’s exploration of 1/3 of the strike length revealed a substantial amount of widespread anomalous gold in soils, and grab samples. Anomalous IP anomalies correlate with the gold and these targets are yet to be drill tested.”

Webster: “Heenan Mallard is located on the SE corner of the large Swayze volcanic pile on a large regional magnetic anomaly that has been hydrothermally altered with gold showings. Heenan is located on the fold nose of the Woman River iron formation that has gold grab samples (0.4 gpt Au) with soil geochem and IP anomalies. This is a very high priority drill target. On the NW corner of the Mallard claim block back in 1958, Noranda drilling intersected economic gold mineralization in multiple drill holes. These intersections require drill follow up. In 1958, gold was $317 an ounce, today it is $1850 per ounce making these drill results very significant. In the SW part of the claim block on the Ridout Shear Zone anomalous soil geochem and grab samples up to 0.7gpt Au were found. This area is ready for drilling.

There are other gold zones on the property that require follow up. The property is located 40 km from IAMGOLD'S Cote lake property where they are building a 35,500 tpd mill (subject to potential increases). IAMGOLD is exploring across the entire Cote Gold land package which including partnerships and joint ventures covers over 600 km2 beyond the Cote Gold mine site.”

The exploration plans for Shining Tree consist of a completion of the program announced in August 2022. The new technical committee will then determine what targets to drill and the size of the program. The drill program will consist of two phases: 1) new targets in the new areas based on results from the work done the last two years, and 2) expanding the Herrick resource and possibly drilling the former Ronda mine located in the central area of the project. According to the geologists there is far greater potential to make new discoveries by looking at the Ridout-Tyrell Deformation Zone (RTDZ).

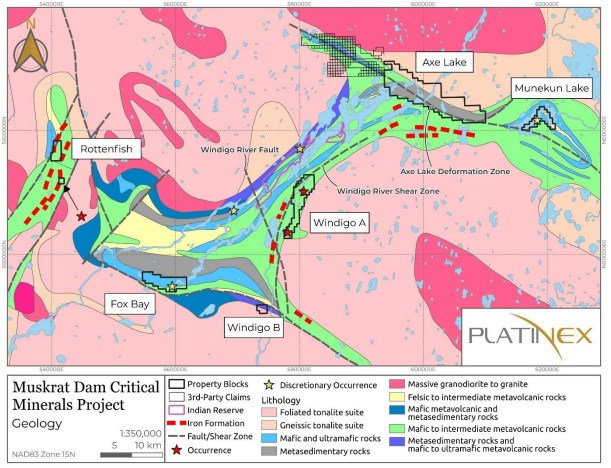

As a reminder, Platinex has two other major projects to explore. Since we are in the middle of a battery metals/lithium boom, I will be following any exploration activity at the Muskrat Dam Project with great interest. Reportedly this will start in April, mapping and sampling the white pegmatites on the Axe Lake property to confirm the presence and grade of lithium mineralization. According to CEO Ferron, a budget for this should be about C$200-300k which will be arranged through the ongoing financings. The program will start with a large sampling program covering the outcrops. After assays the team will begin trenching where the best grades are found and in certain other prospective locations.

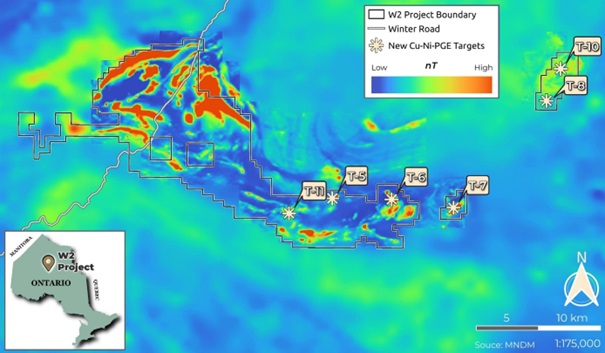

The third project is the W2 Copper-Nickel-PGE project, also in Ontario. Planned exploration consists of infill drilling to establish the continuity of the historically-defined 7.5 km long widely-spaced CuNi-PGE mineralization corridor, and drill testing several high conductance-high magnetic susceptibility geophysical anomalies identified in a 2008 VTEM survey over the eastern portion of W2.

Platinex also plans to carry out a ground gravity survey over the ultramafic intrusion to detect potential chromite mineralization in the northeast part of the western W2 claims, and conducting petrographic and/or preliminary bench-scale metallurgical studies to justify additional drilling along strike of the Fe-Ti-V mineralization in the northwestern part of the W2 claims.

It seems Platinex has a busy exploration year ahead, with substantial programs planned for all three projects.

Conclusion

Since it isn’t easy for a tiny junior like Platinex to explore 3 district scale land packages at the same time, it was a good thing that CEO Ferron leveraged his connections as a board member of Fancamp Exploration, and managed to convince them to invest into a JV, enabling Platinex to finance and able to conduct lots of exploration work at Shining Tree this spring. As Platinex is raising more at very cheap FT prices, there should be plenty of interest, especially since the company has its own potential lithium exploration project now with Muskrat Dam. This could be a hot summer for Platinex. Stay tuned!

I hope you will find this article interesting and useful, and will have further interest in my upcoming articles on mining. To never miss a thing, please subscribe to my free newsletter at www.criticalinvestor.eu, in order to get an email notice of my new articles soon after they are published.

Disclaimer:

The author is not a registered investment advisor, and currently has a long position in this stock. Platinex is a sponsoring company. All facts are to be checked by the reader. For more information go to www.platinex.com and read the company’s profile and official documents on www.sedar.com, also for important risk disclosures. This article is provided for information purposes only, and is not intended to be investment advice of any kind, and all readers are encouraged to do their own due diligence, and talk to their own licensed investment advisors prior to making any investment decisions.

This newsletter/article is not meant to be investment advice, as Criticalinvestor.eu (from now on website, newsletter, and all persons or organisations directly related to it, for example but not limited to: owner, editor, the Seekingalpha author The Critical Investor, publisher, host company, employees, associates, sponsoring companies) is no registered investment advisor. Therefore it is not intended to meet your specific individual investment needs and it is not tailored to your personal financial situation. This newsletter/article reflects the personal and therefore subjective views and opinions of Criticalinvestor.eu and nothing else. The information herein may not be complete, up to date or correct. This newsletter/article is provided in good faith but without any legal responsibility or obligation to provide future updates.

Through use of this website and its newsletter viewing or using you agree to hold Criticalinvestor.eu harmless and to completely release them from any and all liability due to any and all loss (monetary or otherwise), damage (monetary or otherwise), or injury (monetary or otherwise) that you may incur.

You understand that Criticalinvestor.eu could be an investor and/or active trader, meaning that Criticalinvestor.eu could buy and sell certain securities at all times, more specific any or all of the stocks mentioned in own newsletters/articles and other own content like the Watchlist, Leveraged List, etc.

No part of this newsletter/article may be reproduced, copied, emailed, faxed, or distributed (in any form) without the express written permission of Criticalinvestor.eu. Everything contained herein is subject to international copyright protection. The full disclaimer can be found here.